The Frontier of Tax-Aware Investing

Investment strategies designed to materially reduce taxes for eligible investors.

“Taxes are what we pay for a civilized society.”* They fund infrastructure, national defense, legal systems, and public services that make our prosperity possible. But overpaying is optional. There’s no trophy for best taxpayer.

Leading asset managers historically catered mostly to tax-exempt institutional investors like pensions and endowments. Their most sophisticated tax-aware strategies were reserved for ultra-high-net-worth taxable individuals who needing custom solutions. Now, these strategies are available to investors like our clients.

Magnolia Private Wealth keeps pace with this Frontier of Tax-Aware Investing by: identifying which strategies are truly viable, performing due diligence on investment or tax risks, and harnessing those with greatest potential to materially reduce a client’s tax burden–via thoughtful portfolio construction and ongoing management.

Conventional tax-aware tools–the ones most advisors know about–are merely table stakes. What follows sits at the Frontier–strategies that are effective individually and, in combination, produce powerful compounding tax savings.

If you’re a taxable investor, you’re almost certainly paying more taxes than you need to. Magnolia Private Wealth can help you change that—because keeping more of what’s yours is the real trophy.

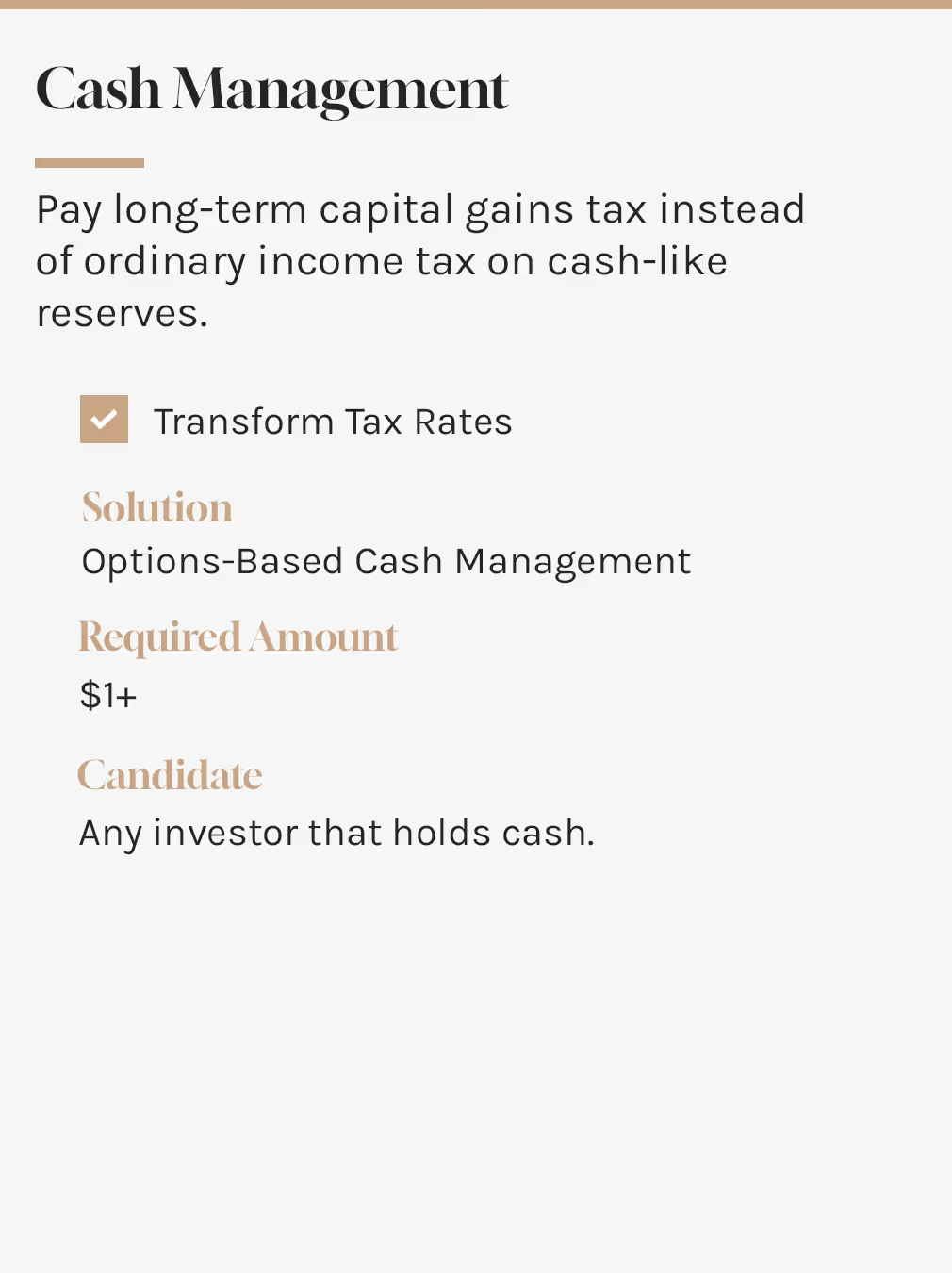

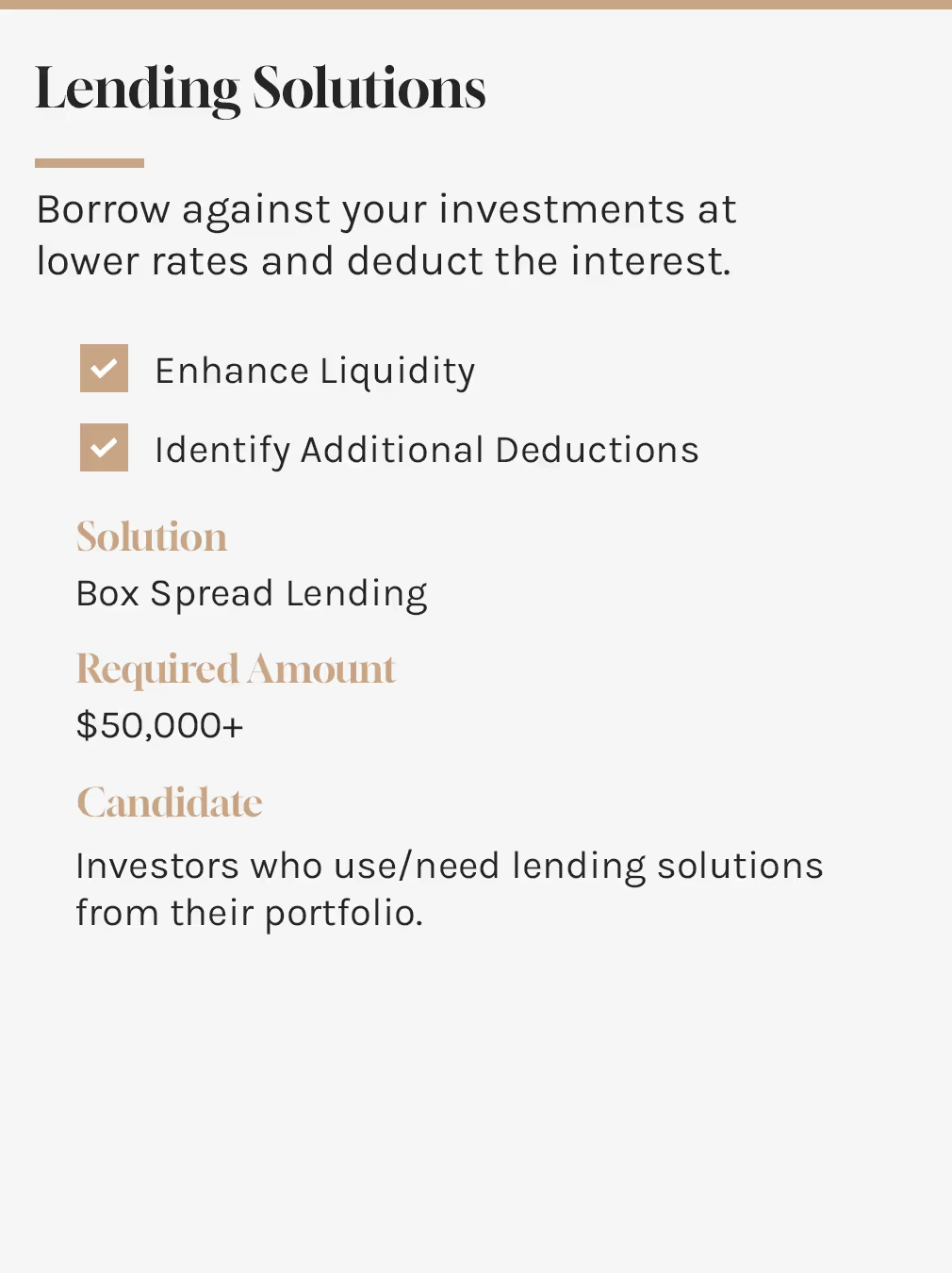

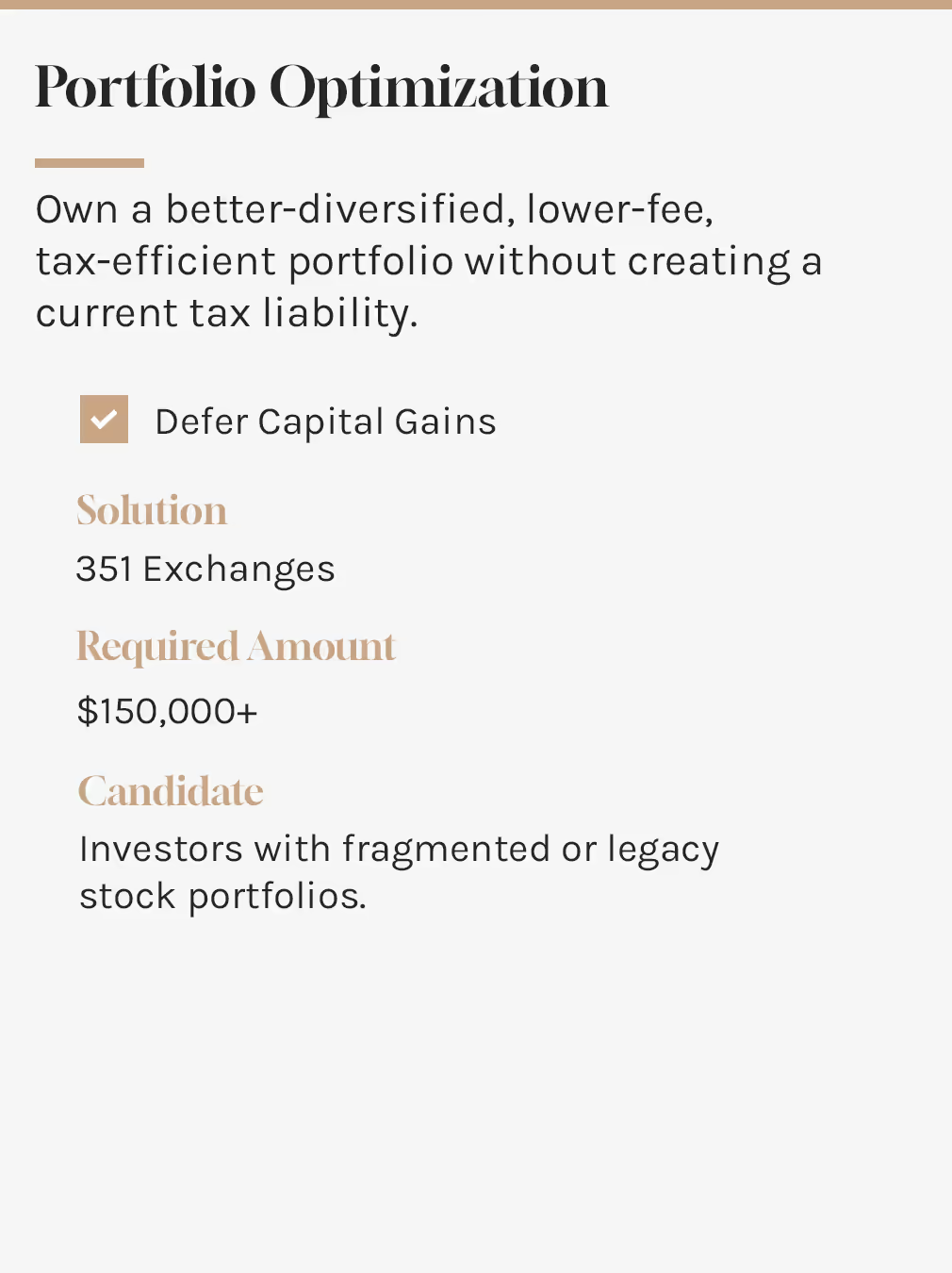

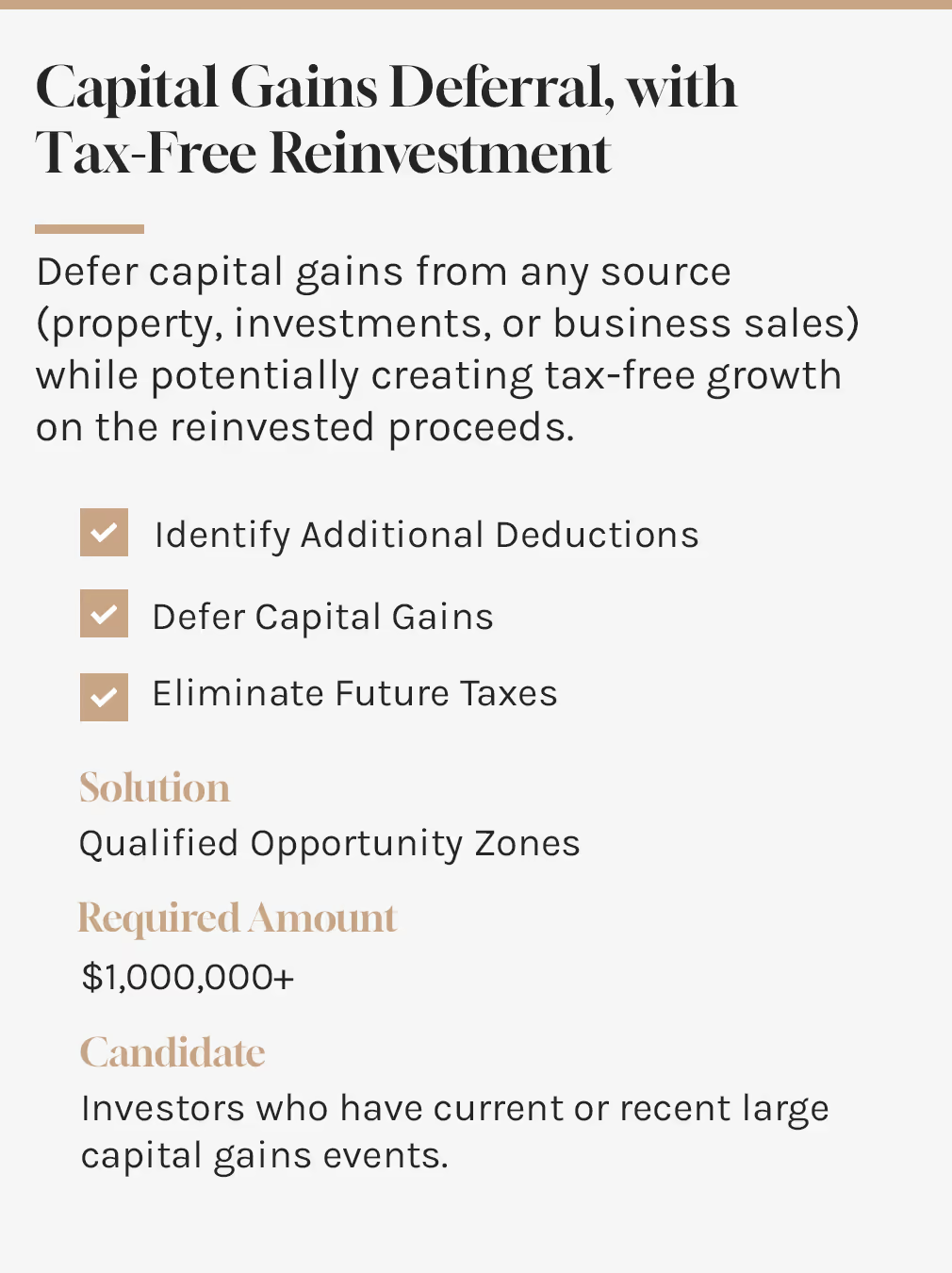

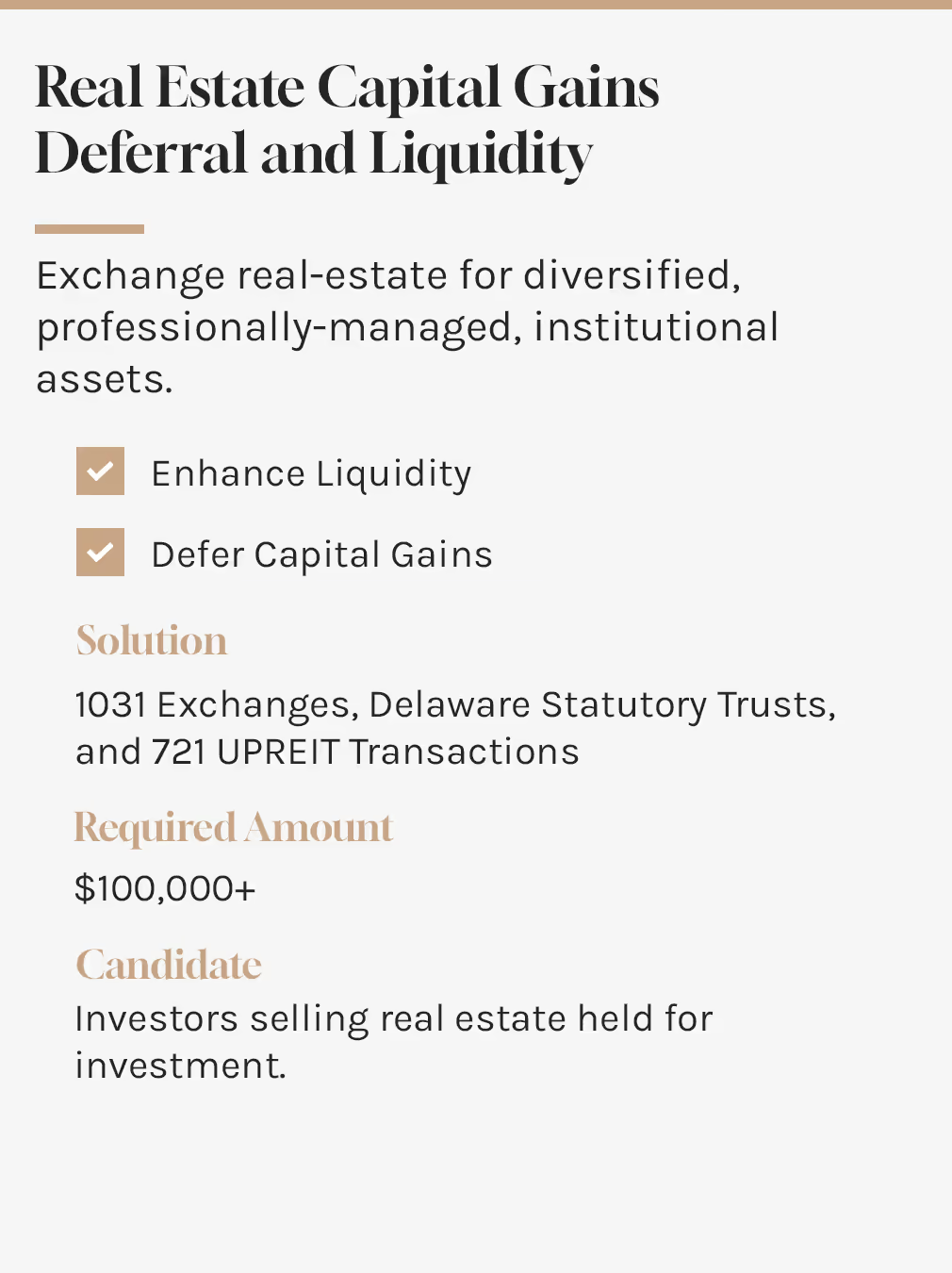

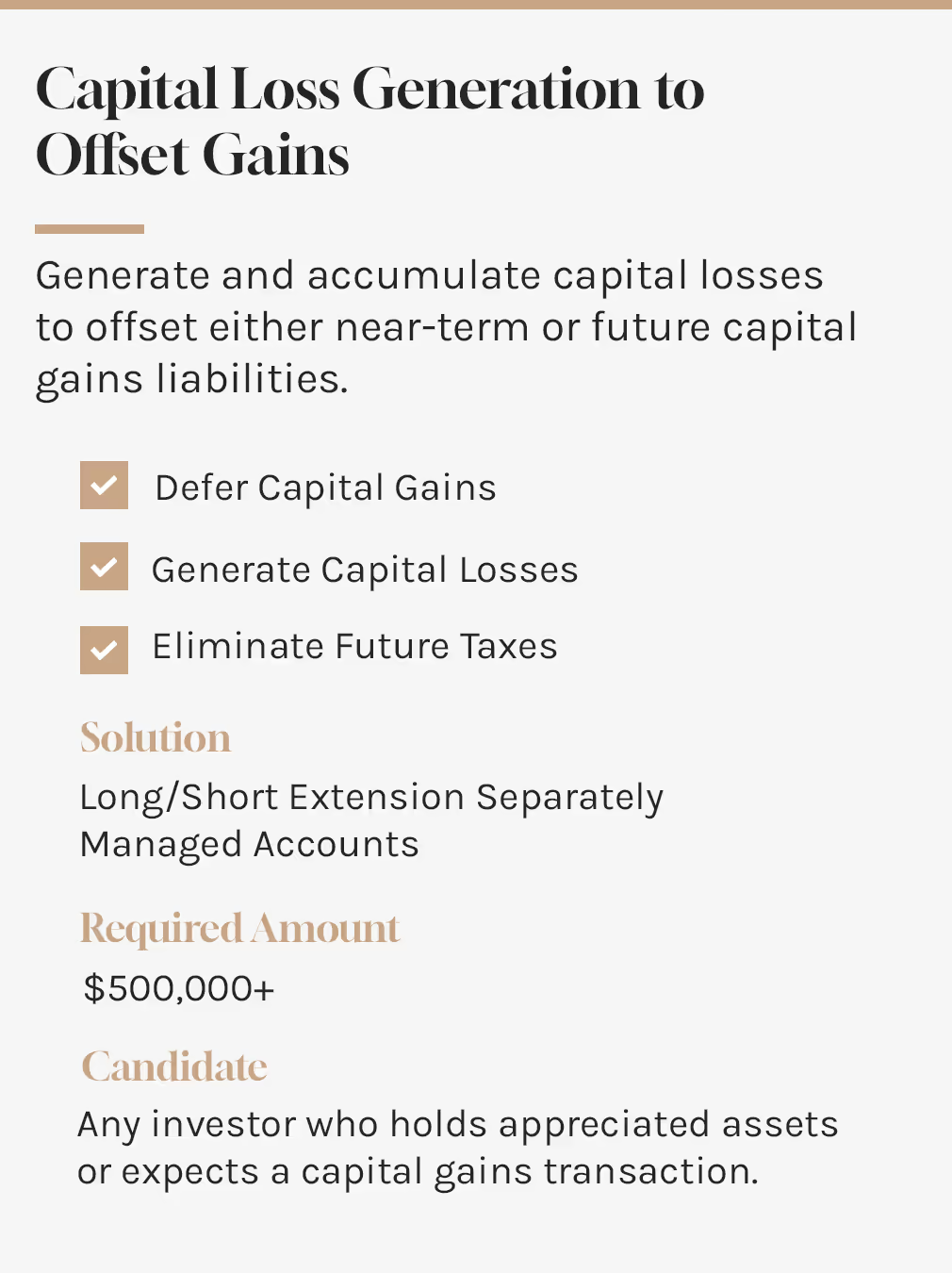

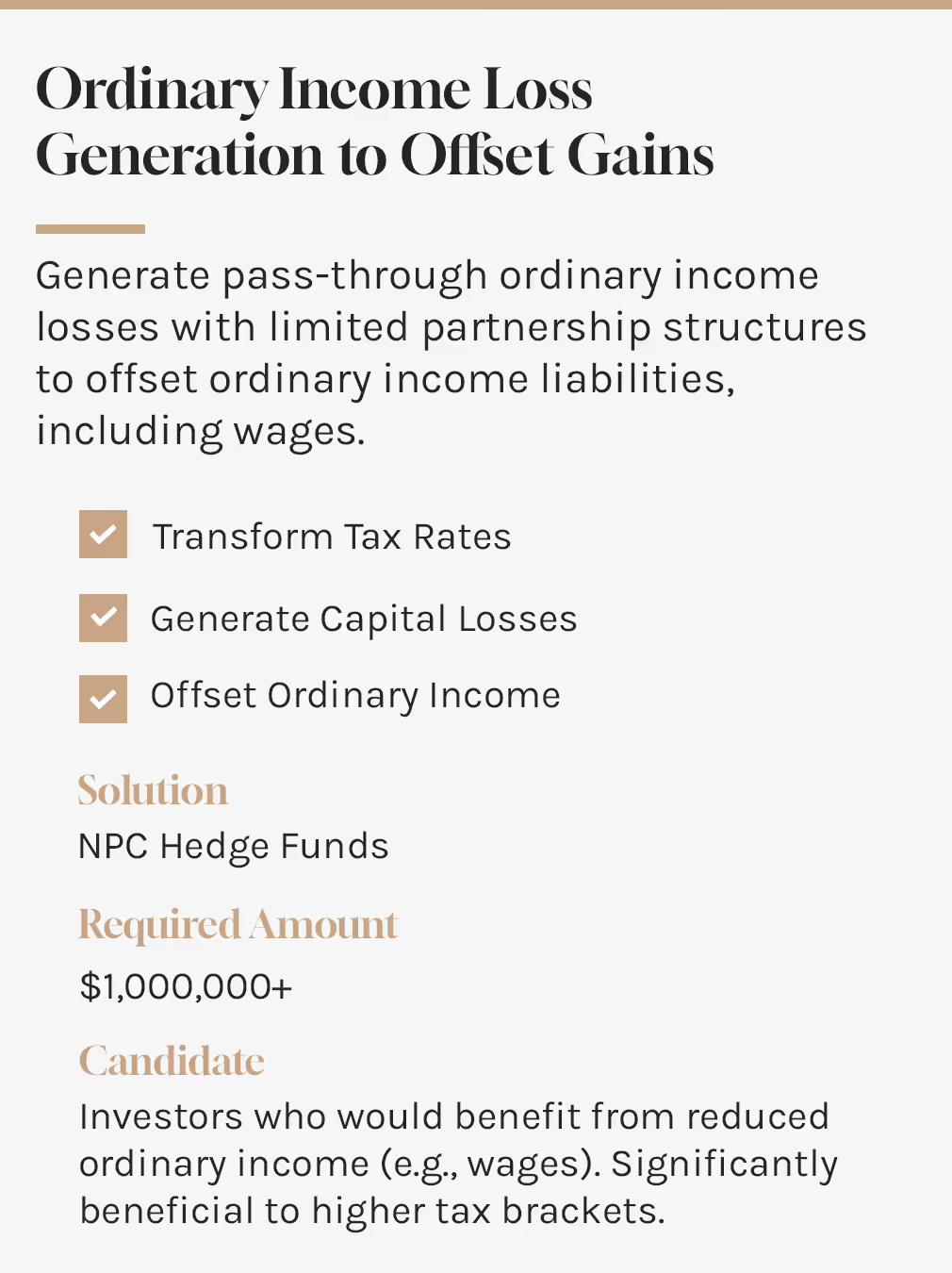

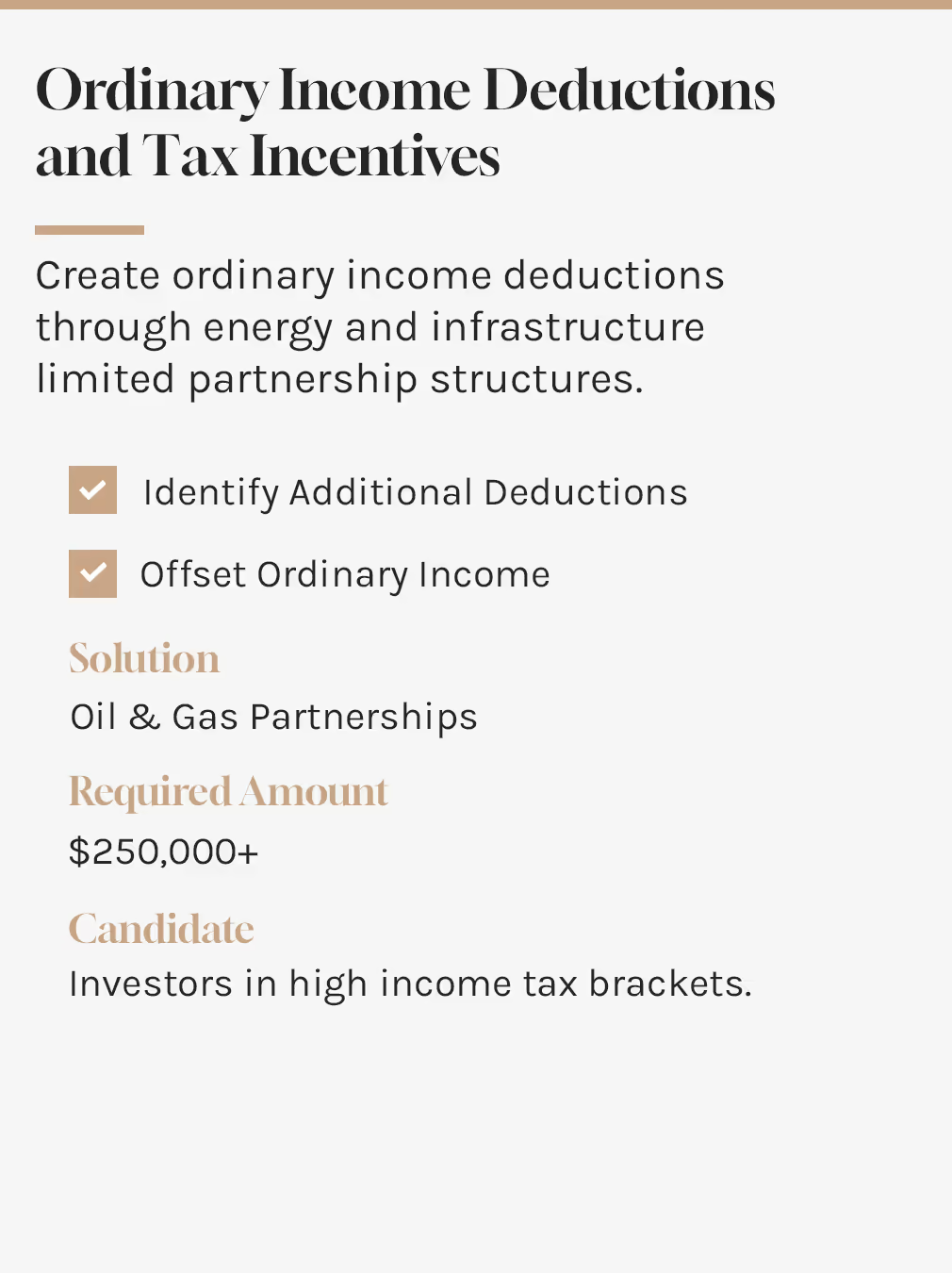

Below are specific opportunities our clients use to reduce their tax liability.

*Oliver Wendell Holmes Jr., US Supreme Court Justice.

These strategies may involve risks and are not suitable for all investors. Magnolia Private Wealth doesn’t provide tax or legal advice; please consult both an investment advisor and coordinate with your tax advisor.

Disclaimer: The opinions voiced and information provided in this document is for informational and educational purposes only. It should not be considered investment, financial, or legal advice. Nothing herein constitutes a recommendation to buy, sell, or hold any security or financial instrument. Magnolia Private Wealth does not provide tax, legal or accounting advice. Investing involves risk, including the potential loss of principal. You should consult with a qualified financial advisor, tax professional, or other appropriate professional before making any financial decisions. The author and publisher assume no liability for any losses or damages resulting from the use of this information.

Insights from Our Team.